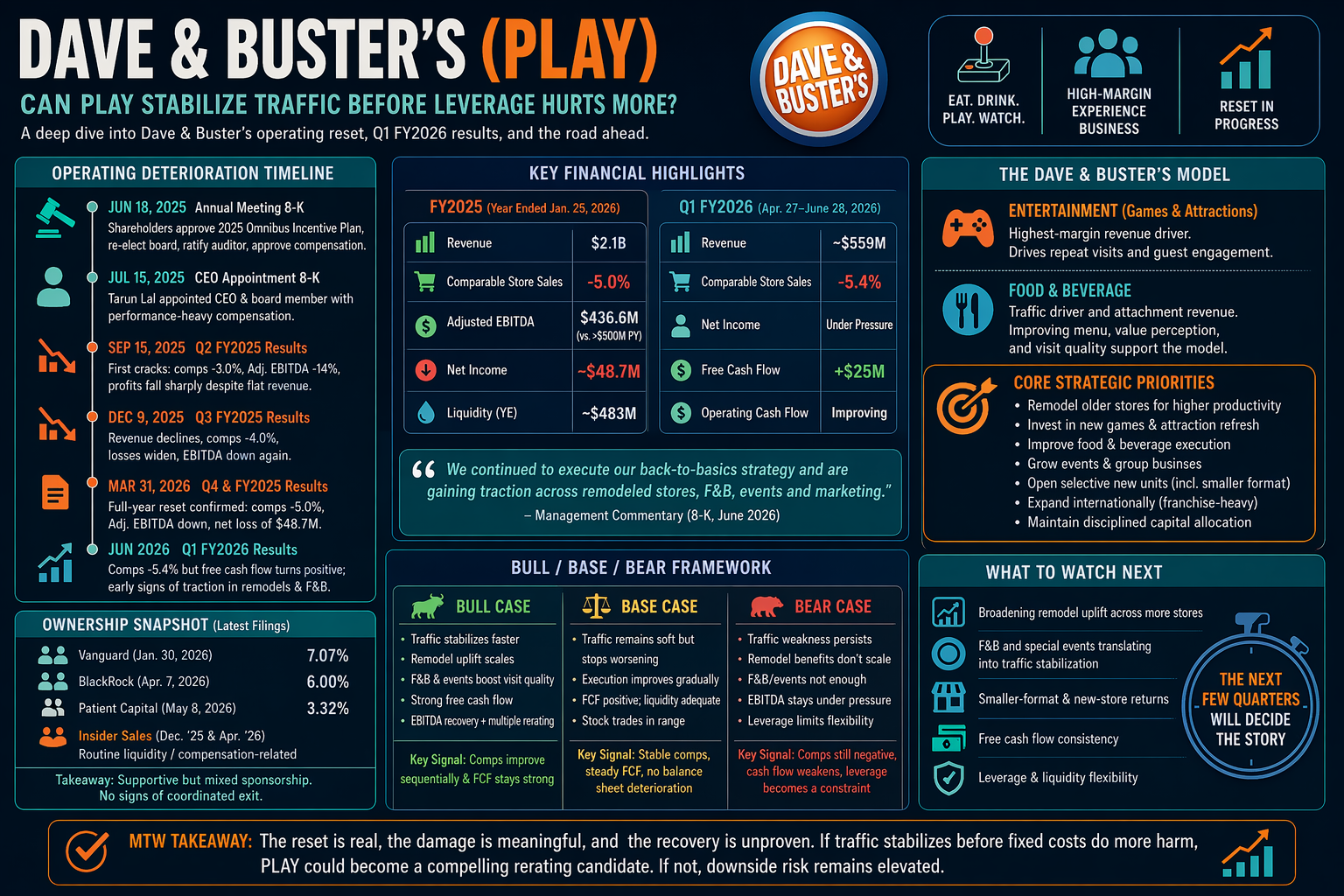

Dave & Buster’s Stock Analysis: Can PLAY Stabilize Traffic Before Leverage Hurts More?

Market Tide Weekly Deep Dive - PLAY

The reset is real. The recovery is unproven. Can PLAY stabilize traffic before leverage does more damage?

The Setup

Dave & Buster’s is best understood as a high-margin experience business in a traffic reset. As Market Tide Weekly recalibrated its pressure to go even deeper this week, Dave & Buster’s became the right place to focus: a company whose filings capture both a real traffic problem and a still-credible case for stabilization. The market is focused on falling comps and earnings compression, but the deeper question is whether remodel-led productivity, tighter capital discipline, and improving cash flow can stabilize the business before fixed costs and leverage make the downturn worse. That is what makes PLAY interesting. The filings show a company that clearly went through a difficult stretch, but they also show why the story is not simply broken: the entertainment-heavy model still offers attractive unit economics, liquidity remains intact, management is still investing through the weakness, and early cash-flow improvement suggests the reset may be gaining traction before traffic has fully recovered. (Dave & Buster’s, 10-K, Mar. 2026) (Dave & Buster’s, 10-Q, June 2026)

The Filing Evidence

The filings show a business that started weakening before headline revenue made the problem obvious. The first meaningful cracks appeared in Q2 2025, when comparable sales turned negative and profitability compressed sharply even though revenue was roughly flat. By Q3, revenue had begun to decline, losses widened, and adjusted EBITDA moved lower, confirming that traffic pressure and fixed-cost leverage were now working together in the wrong direction. The March 31, 2026 earnings filing completed the picture: full-year fiscal 2025 revenue fell to about $2.1 billion, comparable sales were down 5.0%, adjusted EBITDA dropped to roughly $436.6 million from more than $500 million, and the company swung to a net loss of about $48.7 million. (Dave & Buster’s, 8-K, Sept. 2025) (Dave & Buster’s, 8-K, Dec. 2025) (Dave & Buster’s, 8-K, Mar. 2026) (Dave & Buster’s, 10-K, Mar. 2026)

That deterioration matters because PLAY is not a typical restaurant chain. Dave & Buster’s and Main Event operate a large-format entertainment model in which games and attractions generate the highest-margin revenue and food and beverage support traffic and visit quality. That gives the company better underlying unit economics than a standard casual-dining business, but it also means even modest traffic pressure can create large earnings swings because labor, rent, and occupancy costs do not flex down quickly. The first quarter of fiscal 2026 sharpened that tension. Revenue was roughly $559 million, comparable store sales fell 5.4%, and earnings remained under pressure, yet free cash flow improved to positive $25 million, operating cash flow improved, and management continued to describe a “back-to-basics” strategy and say it was “gaining traction” through remodel performance, better food-and-beverage trends, events growth, game refreshes, and tighter capital discipline. (Dave & Buster’s, 10-K, Mar. 2026) (Dave & Buster’s, 10-Q, June 2026) (Dave & Buster’s, 8-K, June 2026)

The Opportunity / Risk

The most important thing to understand about PLAY is that the market is reacting to the right problem, but not necessarily to the full shape of the opportunity. The right problem is traffic. Comparable sales are negative, guest demand is softer, and this is a fixed-cost business where even small changes in guest counts can produce outsized changes in earnings. That is the core reason profits collapsed so quickly from Q2 through year-end, and it remains the central risk going forward. This is no longer a growth story; it is a stabilization story. But the business does not need to become a growth story again to improve. It needs to stabilize, protect cash flow, and prove that remodel-led productivity and tighter execution can stop the earnings damage from compounding.

That is the constructive side of the thesis. PLAY is still a high-margin experience business, and the filings suggest management is trying to improve both traffic quality and capital efficiency at the same time. Remodels matter because they can directly change guest engagement and store productivity. Smaller-format stores matter because they can improve returns on invested capital, even if they remain more a promising strategic lever than proven evidence of better unit economics at scale. Food-and-beverage momentum matters because it can improve value perception and visit quality. And free cash flow matters most of all because it gives management time to prove that the traffic problem is cyclical and fixable rather than structural. Governance and ownership help at the margin: the board appears relatively shareholder-friendly, incentives are tied to turnaround metrics, and Vanguard and BlackRock still signal meaningful passive sponsorship even if Patient Capital’s trimming and routine insider liquidity add some caution. The proxy’s incentive design looks directionally strong and aligned with the right turnaround metrics, but it still does not count as proof that execution is improving. The CEO transition has clearly improved strategic clarity and alignment, but it still has not produced broad hard proof of execution improvement in systemwide traffic or operating results. Added board expertise improves the credibility of oversight, but it still does not count as hard evidence of better capital allocation or stronger operating outcomes. Food-and-beverage gains, special-events growth, and remodeled-store uplift all suggest improving traffic quality, but they still stop short of proving broad systemwide traffic recovery while comparable sales remain negative. Leverage does not yet look like an immediate solvency problem, but it still meaningfully reduces downside flexibility if traffic recovery slips. None of that rescues the thesis, but it does support the idea that the story is stressed rather than broken. The bull case is that PLAY does not need a full return to growth to work. It only needs traffic to stop worsening fast enough for the high-margin entertainment mix, improving cash flow, and better execution to start working in its favor again. The bear case is that traffic does not stabilize in time. If consumer softness lingers, remodel benefits fail to scale, and food-and-beverage or events gains remain too narrow, the company could stay stuck in soft comps, compressed EBITDA, pressured cash generation, and a balance sheet with little room for error. (Dave & Buster’s, 10-K, Mar. 2026) (Dave & Buster’s, DEF 14A, May 2026) (Dave & Buster’s, 8-K, May 2026) (Dave & Buster’s, Schedule 13G/A, Jan. 2026) (Dave & Buster’s, Schedule 13G/A, Apr. 2026) (Dave & Buster’s, Schedule 13G/A, May 2026) (Dave & Buster’s, Form 144, Dec. 2025) (Dave & Buster’s, Form 144, Apr. 2026)

Risks to the Thesis

The main risk is that traffic does not stabilize in time. Consumer softness may last longer than management expects, remodel benefits may not scale, and food-and-beverage or events gains may prove too narrow to change the broader demand trend. If that happens, the company could stay stuck in soft comps, compressed EBITDA, pressured cash generation, and a balance sheet with little room for error.

PLAY in focus: traffic is falling, cash flow is improving—and the next few quarters will determine whether this reset turns into a real recovery.

What Matters Most From Here

What matters most from here is whether the company can stabilize the business before the fixed-cost structure does further damage. The key signals are whether remodel uplift broadens, whether food-and-beverage and special-events gains translate into broader traffic stabilization, whether smaller-format and new-store investments improve returns, and whether free cash flow remains strong enough to give management flexibility while the turnaround is still incomplete. If those indicators improve together, the PLAY story becomes more than a turnaround narrative. If they do not, the market’s skepticism will remain justified.

MTW Bottom Line

Dave & Buster’s is best understood as a high-margin experience business in a traffic reset. The market is focused on falling comps and earnings compression, but the more important question is whether remodel-led productivity, tighter capital discipline, and improving cash flow can stabilize the business before fixed costs and leverage make the downturn worse. The filings suggest that the reset is real, the damage has already been meaningful, and the recovery is still unproven. But they also suggest that if traffic stabilizes before the fixed-cost structure does further harm, PLAY could become a more compelling rerating candidate than the recent headline numbers imply. If management fails to broaden the current improvement signals or if consumer weakness persists longer than expected, that more constructive outcome could fade quickly. (Dave & Buster’s, 10-K, Mar. 2026) (Dave & Buster’s, 10-Q, June 2026) (Dave & Buster’s, DEF 14A, May 2026)

REQUIRED DISCLOSURE — REPRODUCTION IN FULL IS MANDATORY

"Market Tide Weekly is for informational and educational purposes only. Nothing in this newsletter constitutes investment advice, a solicitation to buy or sell any security, or a guarantee of any outcome. Past performance of featured picks is not indicative of future results. All investing involves risk, including the possible loss of principal. Readers should conduct their own due diligence and consult a qualified financial advisor before making investment decisions. Market Tide Weekly and its operators may hold positions in securities discussed."

Works Cited

Dave & Buster’s Entertainment, Inc. Form 8-K. 15 Sept. 2025.

Dave & Buster’s Entertainment, Inc. Form 8-K. 9 Dec. 2025.

Dave & Buster’s Entertainment, Inc. Form 8-K. 31 Mar. 2026. Accession No. 0001525769-26-000006.

Dave & Buster’s Entertainment, Inc. Form 10-K. 31 Mar. 2026. Accession No. 0001525769-26-000008.

Dave & Buster’s Entertainment, Inc. Form 10-Q. June 2026.

Dave & Buster’s Entertainment, Inc. DEF 14A. 6 May 2026. Accession No. 0001525769-26-000018.

Dave & Buster’s Entertainment, Inc. Form 8-K. 1 May 2026. Accession No. 0001525769-26-000010.

Dave & Buster’s Entertainment, Inc. Schedule 13G/A. 30 Jan. 2026.

Dave & Buster’s Entertainment, Inc. Schedule 13G/A. 7 Apr. 2026.

Dave & Buster’s Entertainment, Inc. Schedule 13G/A. 8 May 2026.

Dave & Buster’s Entertainment, Inc. Form 144. 18 Dec. 2025.

Dave & Buster’s Entertainment, Inc. Form 144. 17 Apr. 2026.