PRTA After the 2025 Shakeout: Cash, Catalysts, Concentrated Holders, and the Capital Strategy Behind the Move

Market Tide Saturday Special Edition — PRTA After the 2025 Shakeout

PRTA after the shakeout: strong cash, real catalysts, and a capital strategy built for uncertainty.

Edition Type: Market Tide Saturday Special Edition

Subject: Prothena Corporation plc (PRTA)

Investor Summary

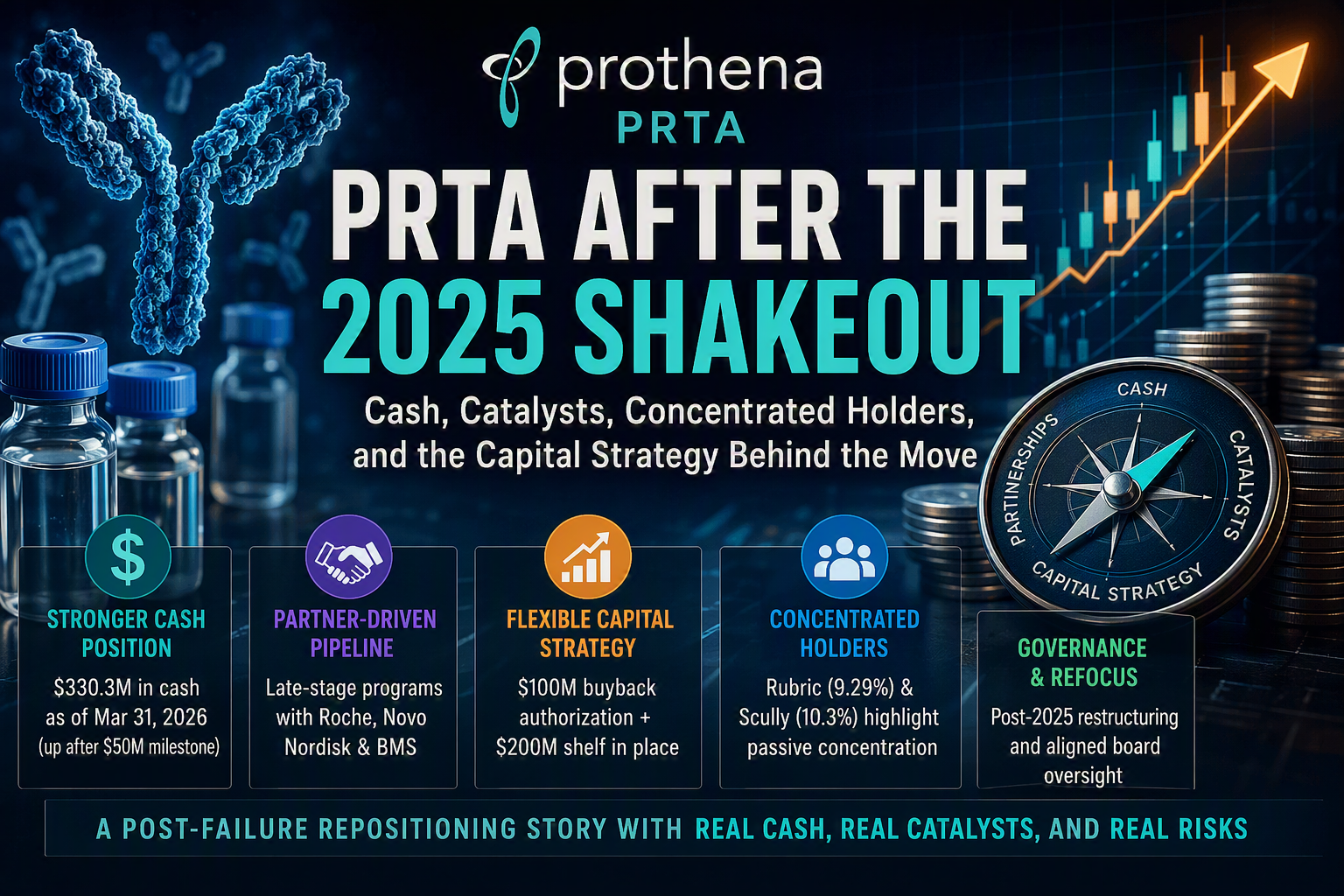

· The core thesis: PRTA is no longer just a development-stage biotech with a quarterly milestone beat; it is a post-failure repositioning story built around cash position, partner-driven milestones, concentrated passive ownership, and an unusually flexible capital toolkit. (Prothena, 10-K, Feb. 2026; Prothena, 10-Q, May 2026; Prothena, 8-K, Feb. 2026; Prothena, POS AM, Feb. 2026)

· The opportunity: A stronger cash position, no-debt balance-sheet framing, potential partner milestones, and late-stage programs advanced by Roche, Novo Nordisk, and Bristol Myers Squibb give PRTA multiple ways to rebuild credibility after the 2025 clinical setback and restructuring. (Prothena, 10-K, Feb. 2026; Prothena, 10-Q, May 2026)

· The risk: Q1 profitability was milestone-driven, not recurring; future value still depends on external partners, clinical execution, milestone timing, capital-allocation discipline, and the behavior of a concentrated holder base. (Prothena, 8-K, May 2026; Prothena, 10-Q, May 2026; Prothena, Schedule 13G/A, May 2026)

Key Findings Summary

· PRTA’s financial profile improved sharply in Q1 2026, but the improvement was milestone-driven. The company’s $51.1 million revenue quarter and $32.7 million net income were anchored by a $50 million Novo Nordisk milestone rather than recurring commercial revenue. That makes the quarter important, but not automatically repeatable. (Prothena, 10-Q, May 2026; Prothena, 8-K, May 2026)

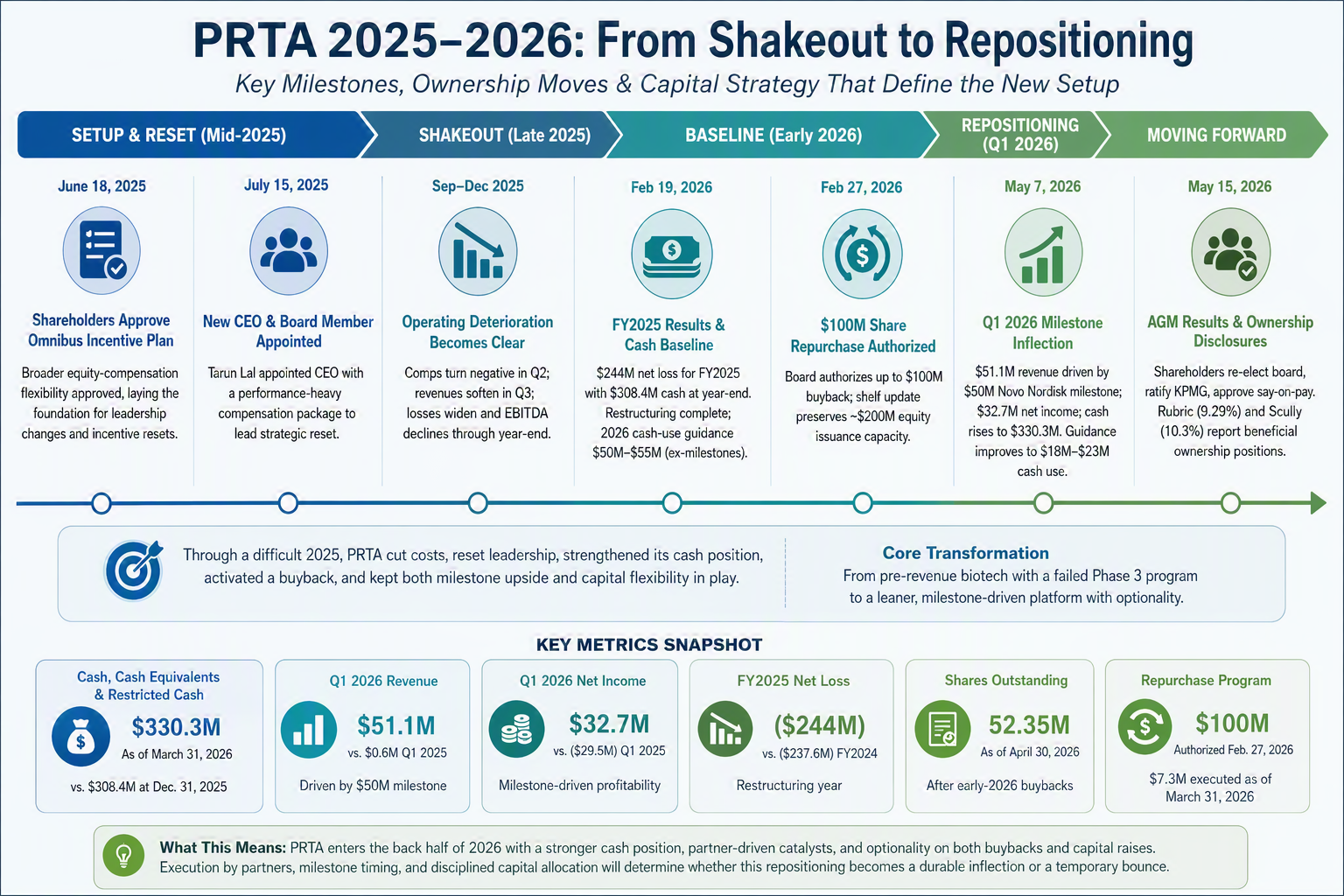

· The company entered 2026 with a strong cash position, but the annual baseline still showed material losses and cash burn. PRTA ended 2025 with approximately $308.4 million in cash and restricted cash after using $163.7 million in operating and investing activities during the year, while FY2025 net loss was approximately $244 million. The Q1 milestone improved the cash outlook, but liquidity should still be viewed as near-term support rather than evidence of a self-funding model. (Prothena, 8-K, Feb. 2026; Prothena, 10-K, Feb. 2026; Prothena, 10-Q, May 2026)

· The strategic model has shifted toward partner-driven value creation. The forward pipeline story is centered on partnered programs with Roche, Novo Nordisk, and Bristol Myers Squibb, which gives PRTA access to external development resources but also leaves key catalyst timing outside the company’s full control. (Prothena, 10-K, Feb. 2026)

· Capital strategy is bidirectional. Shareholders approved the creation of distributable reserves in November 2025, the board later authorized a $100 million buyback, and the company preserved future equity-issuance flexibility through a shelf update. PRTA can support the stock through repurchases, but it also retains dilution capacity if capital needs or market conditions change. (Prothena, 8-K, Nov. 2025; Prothena, 8-K, Feb. 2026; Prothena, POS AM, Feb. 2026)

· Ownership concentration is a major market-structure factor. Rubric and Scully disclosures together point to a large passive-holder base, which may reduce effective float and amplify reactions to clinical, milestone, governance, or capital-markets events. Passive does not mean irrelevant. (Prothena, Schedule 13G/A, May 2026)

· Governance appears stable, but the post-2025 context still matters. Recent filings show routine shareholder process, clean board-transition language, and approved AGM proposals; however, the proxy materials also frame PRTA as a company still rebuilding after a major clinical and organizational setback. (Prothena, 8-K, Dec. 2025; Prothena, DEF 14A, Mar. 2026; Prothena, DEFA14A, Mar. 2026; Prothena, 8-K, May 2026)

· The central investment question is whether the new operating model is becoming durable. PRTA’s setup only strengthens if milestone flow, partner execution, expense discipline, and capital allocation remain aligned. If those elements break down, the same structure that creates upside sensitivity could also intensify downside volatility.

Why This Saturday Special Matters

A catalyst-driven, capital-structured system where cash, partners, and ownership shape non-linear outcomes.

Every so often, a company’s sequence of disclosures stops looking like a routine update and starts looking like a map. PRTA has reached that point. The company’s recent disclosures tell a coherent story: a major clinical setback in 2025, a leaner operating structure, a well-funded but still cash-consuming balance sheet, a partner-driven pipeline, a shareholder-approved capital-return framework, a $100 million buyback authorization, a shelf that preserves dilution capacity, and a large passive ownership base that could make the stock highly sensitive to catalysts. (Prothena, DEF 14A, Mar. 2026; Prothena, 10-K, Feb. 2026; Prothena, 8-K, Nov. 2025; Prothena, 8-K, Feb. 2026; Prothena, POS AM, Feb. 2026; Prothena, Schedule 13G/A, May 2026)

That is why PRTA deserves a Market Tide Saturday Special Edition instead of a standard company update. The story is not simply “the company had a good quarter.” The better question is whether PRTA has entered a structurally stronger cash-and-catalyst phase after a painful restructuring, or whether the market is at risk of overreading a milestone-heavy quarter as normalized operating strength.

The Setup: A Repositioning Story, Not a Normal Growth Story

The current setup only makes sense in the context of how PRTA got here:

From setback to setup: PRTA’s 2025 shakeout reshaped the business into a leaner, milestone-driven structure with renewed capital flexibility.

PRTA entered 2026 with the financial profile of a company that still had meaningful cash consumption, but also enough balance-sheet strength to avoid the usual near-term desperation that often defines clinical-stage biotechnology companies. The February 2026 baseline showed approximately $308.4 million of cash, cash equivalents, and restricted cash at year-end 2025, against $163.7 million of net cash used in operating and investing activities during the year. The annual revenue base was limited: FY2025 revenue was approximately $9.7 million, down sharply from approximately $135 million in 2024, reinforcing that PRTA was not operating as a recurring-revenue story. Management’s original 2026 guidance called for $50 million to $55 million of net cash use and roughly $255 million of year-end cash at the midpoint, excluding potential partner milestones. (Prothena, 8-K, Feb. 2026; Prothena, 10-K, Feb. 2026)

The FY2025 expense base also shows why the restructuring matters. In FY2025, operating expenses were approximately $224 million, including $134.9 million of R&D expense, $59.4 million of G&A expense, and $30.1 million of restructuring expense. PRTA reported an approximately $244 million net loss for the year, so the company entered 2026 with liquidity but not with a self-funding operating model. The company’s guidance pointed to adequate near-term cash coverage, while the loss profile and milestone-dependent model mean future financing choices remain relevant to the investment case. (Prothena, 10-K, Feb. 2026)

That baseline matters because it frames everything that followed. PRTA was not starting from weakness, but it was not operating from recurring product revenue either. Its value path had narrowed toward partnership economics, milestone receipts, and long-dated clinical outcomes. The 2025 restructuring — including the discontinuation of birtamimab after a failed Phase 3 trial and the approximately 63% workforce reduction described in company materials — makes the current setup less about traditional operating growth and more about whether the company can convert a smaller platform into partner-driven value creation. (Prothena, 10-K, Feb. 2026; Prothena, DEF 14A, Mar. 2026)

The Financial Evidence: Cash Profile Improved, But the Quality of Revenue Matters

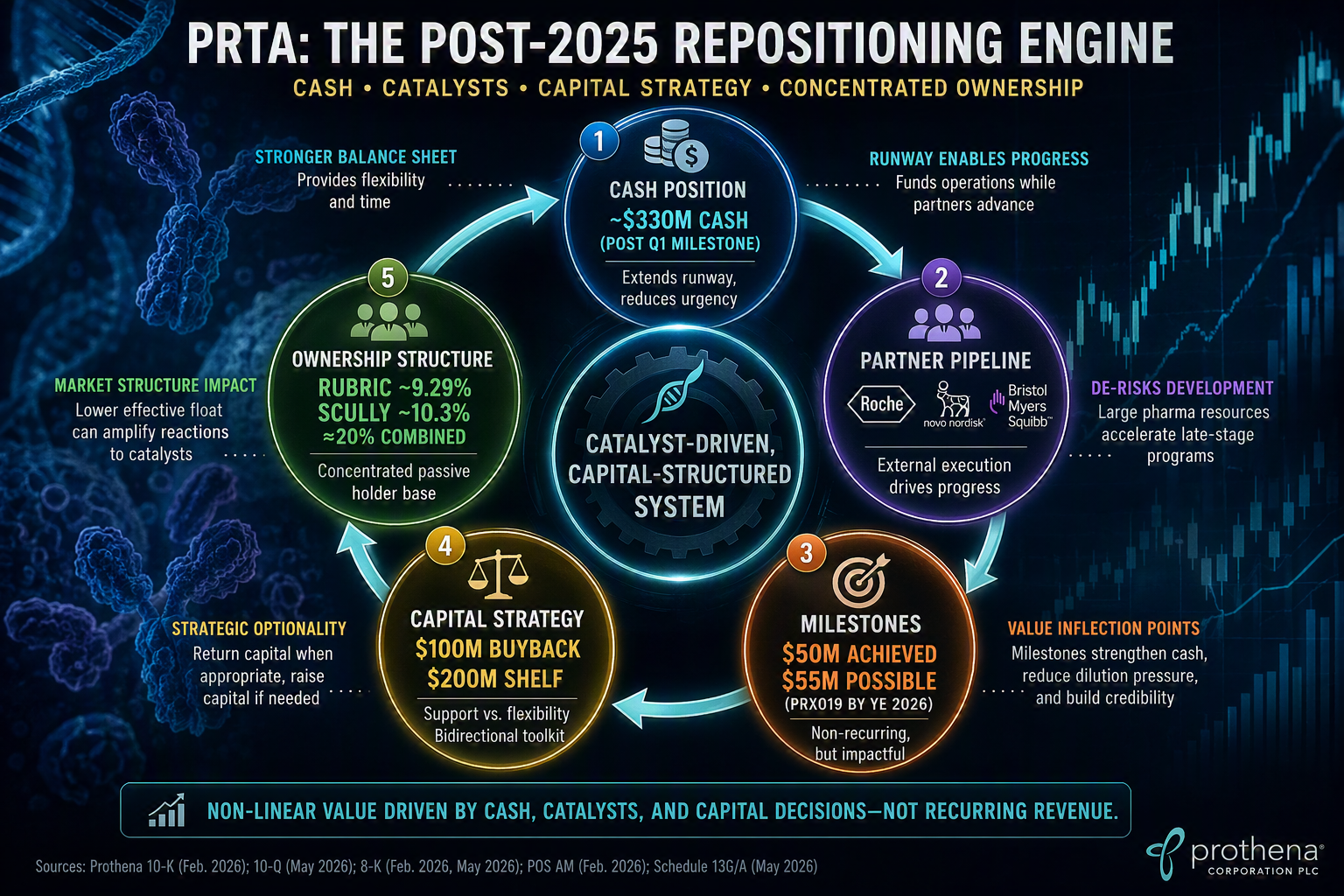

The Q1 2026 financial update changed the tone of the story. PRTA reported approximately $51.1 million in quarterly revenue and approximately $32.7 million in net income, compared with a much weaker prior-year period. On a per-share basis, the quarter translated to basic EPS of $0.61 and diluted EPS of $0.60, reinforcing how much the milestone shifted reported profitability for the period. The main driver was a $50 million clinical milestone payment from Novo Nordisk tied to coramitug Phase 3 enrollment. PRTA also generated approximately $28.9 million of net cash provided by operating and investing activities during Q1 2026, a sharp contrast to the $163.7 million of full-year 2025 net cash used in operating and investing activities. That milestone-driven cash inflow helped push cash, cash equivalents, and restricted cash to approximately $330.3 million at March 31, 2026, including approximately $329.5 million of cash and cash equivalents and $0.9 million of non-current restricted cash. Total liabilities also declined to approximately $37.3 million at March 31, 2026 from approximately $46.3 million at December 31, 2025, and company disclosures indicate no debt, reinforcing that the balance-sheet improvement was not limited to cash. (Prothena, 10-Q, May 2026; Prothena, 8-K, May 2026)

On the surface, the quarter looked like a sharp financial inflection. But the quality of that inflection matters. This was not evidence that PRTA had suddenly become a recurring-revenue business. It was evidence that milestone economics can materially change the company’s cash profile when partner programs advance. Management’s updated 2026 guidance reflected that shift: expected net cash use improved to $18 million to $23 million, and expected year-end cash rose to approximately $273 million at the midpoint. (Prothena, 10-Q, May 2026; Prothena, 8-K, May 2026)

The cost structure also showed the effect of the post-2025 restructuring. Q1 2026 R&D expense declined to approximately $12.6 million from $50.8 million in the prior-year quarter, while G&A expense declined to approximately $12.7 million from $17.6 million. PRTA also recorded an approximately $4.2 million restructuring credit, which improves the quarter but should not be treated as a durable operating run-rate item without follow-up confirmation. (Prothena, 10-Q, May 2026; Prothena, 8-K, May 2026)

The right interpretation is therefore balanced. PRTA’s balance sheet looks stronger after Q1, and the company has more flexibility than it did entering the year. But investors should not treat a milestone-driven profit quarter, a restructuring credit, or a temporarily positive cash-flow period as normalized operating profitability. The investment case depends on whether additional partner milestones, clinical progress, and disciplined capital allocation can extend the runway without eroding the shareholder base.

The Partner Pipeline: Upside Is Real, But It Is Externally Controlled

Prothena’s filings point to three major partnered programs as the center of gravity. Roche initiated the Phase 3 PARAISO trial for prasinezumab in early-stage Parkinson’s disease, and Novo Nordisk initiated the Phase 3 CLEOPATTRA trial for coramitug in ATTR amyloidosis with cardiomyopathy. Bristol Myers Squibb has fully enrolled the Phase 2 TargetTau-1 trial evaluating BMS-986446 in early Alzheimer’s disease, while PRX019 has completed Phase 1 and remains subject to a Bristol Myers Squibb advancement decision that could trigger a potential $55 million milestone by year-end 2026. Management had identified up to $105 million of possible 2026 aggregate clinical milestones tied to coramitug and PRX019; after the $50 million Novo Nordisk coramitug milestone was achieved in Q1, the main remaining disclosed milestone watch item was the potential $55 million Bristol Myers Squibb PRX019 milestone. (Prothena, 10-K, Feb. 2026; Prothena, 8-K, Feb. 2026; Prothena, 10-Q, May 2026)

This is both the appeal and the limitation of the PRTA setup. The company can benefit from large-pharma execution without funding every program internally. That gives it optionality. But it also means PRTA does not fully control its own timing. The most important late-stage programs are partner-led, and some key trial completions are long-dated. Near-term valuation sensitivity is therefore more likely to come from milestones, regulatory designations, partner decisions, interim updates, and market interpretation than from commercial revenue.

The Capital Strategy: Buyback Support and Dilution Flexibility Exist Side by Side

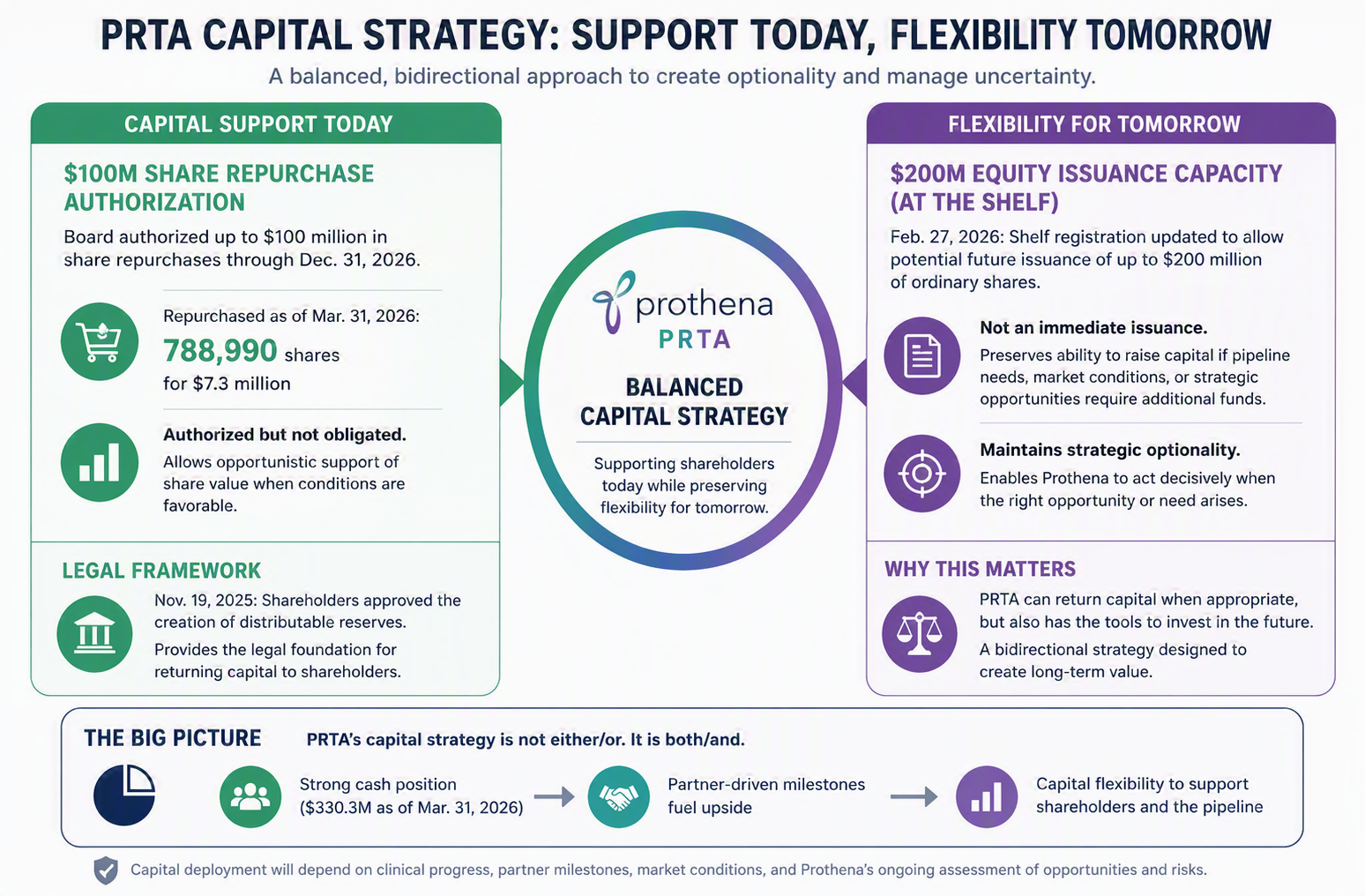

The capital strategy is one of the most important parts of the story. In November 2025, shareholders approved a capital reduction to create distributable reserves. That vote appears to have created the legal framework for future capital returns under Irish corporate law. The proposal passed overwhelmingly, with roughly 37.8 million votes in favor and minimal opposition. (Prothena, 8-K, Nov. 2025)

Then, in February 2026, the board authorized a discretionary share repurchase program of up to $100 million, expected to run through December 31, 2026. By March 31, 2026, PRTA had repurchased 788,990 ordinary shares for $7.3 million, leaving most of the authorization unused if measured against the original program size. The company also reported 52,353,237 ordinary shares outstanding as of April 30, 2026, making both repurchase activity and future issuance capacity relevant to the share-count debate. That does not guarantee future buybacks, but it does show that the authorization was not merely theoretical. (Prothena, 8-K, Feb. 2026; Prothena, 10-Q, May 2026)

At the same time, PRTA preserved the other side of the capital toolkit. A February 2026 post-effective amendment updated the company’s shelf registration framework, creating potential future equity-issuance capacity of approximately $200 million of ordinary shares. That filing did not represent an immediate issuance, but it matters because it places dilution flexibility next to buyback flexibility. (Prothena, POS AM, Feb. 2026)

PRTA’s capital strategy balances shareholder support today with the flexibility to raise capital as future needs evolve.

This creates PRTA’s bidirectional capital strategy: management can return capital if valuation and cash conditions support it, but it can also raise equity if pipeline needs, market conditions, or strategic timing require more capital. The practical financial tension is that the company had enough cash to repurchase shares after the workforce reduction, yet it also preserved approximately $200 million of potential ordinary-share issuance capacity. That duality isn’t a contradiction; it is how PRTA manages uncertainty.

The Ownership Structure: Passive Does Not Mean Irrelevant

The ownership disclosures add another layer. Rubric Capital Management LP and David Rosen disclosed 5,000,000 ordinary shares, or approximately 9.29% beneficial ownership, in a May 2026 Schedule 13G/A. William P. Scully disclosed 5,378,846 ordinary shares, or approximately 10.3% beneficial ownership, in a May 2026 Schedule 13G/A. Together, those disclosed positions point to meaningful passive-holder concentration around PRTA’s post-2025 transition. (Prothena, Schedule 13G/A, May 2026)

The important point is not that these holders are activist. They are reported through passive ownership filings. The important point is that passive holders can still shape trading behavior. A concentrated holder base can reduce effective float, magnify reactions to milestones, and create supply risk if large holders trim or exit. In a catalyst-driven biotech, that matters.

This is why PRTA’s stock may not respond only to fundamentals in a linear way. It may respond to how a small number of large holders reposition around partner decisions, clinical updates, capital actions, and sentiment shifts. That is a market-structure point, not a prediction.

The Governance Layer: Stable Process After a Difficult Year

The governance record looks more stable than the operating history. A December 2025 board resignation appears clean, with no stated disagreement. The March 2026 proxy materials show routine shareholder process and a compensation system heavily weighted toward performance, equity, and retention after restructuring. The May 2026 AGM results show shareholders re-elected directors, ratified KPMG, and approved named executive officer compensation on an advisory basis. (Prothena, 8-K, Dec. 2025; Prothena, DEF 14A, Mar. 2026; Prothena, DEFA14A, Mar. 2026; Prothena, 8-K, May 2026)

That does not eliminate governance risk. Incentive-heavy compensation after a large loss-making year and major restructuring deserves scrutiny. But the public record does not show an obvious activist challenge, failed vote, or contested governance process. The better interpretation is that PRTA has concentrated ownership and a stable formal governance process, which puts more pressure on execution rather than governance drama.

Risk Map

· Milestone quality risk: Q1 profitability was driven by a partner milestone rather than recurring commercial revenue. (Prothena, 10-Q, May 2026; Prothena, 8-K, May 2026)

· Partner execution risk: Roche, Novo Nordisk, and Bristol Myers Squibb control important parts of the forward catalyst path. (Prothena, 10-K, Feb. 2026)

· Clinical timing risk: Key late-stage programs are long-dated, and interim developments may drive sentiment before definitive outcomes. (Prothena, 10-K, Feb. 2026)

· Capital allocation and liquidity risk: PRTA entered 2026 with meaningful cash, but FY2025 net loss was approximately $244 million and the company’s milestone-dependent model means future financing choices remain relevant. The company can buy back shares, but it can also issue equity through shelf capacity if conditions warrant. (Prothena, 10-K, Feb. 2026; Prothena, 8-K, Feb. 2026; Prothena, POS AM, Feb. 2026)

· Ownership concentration risk: Large passive holders may support the setup, but their selling could create pressure quickly. (Prothena, Schedule 13G/A, May 2026)

· Post-2025 credibility risk: The clinical failure and workforce reduction remain central context for how investors evaluate management execution. (Prothena, DEF 14A, Mar. 2026; Prothena, 10-K, Feb. 2026)

What We’re Watching Next

· Whether Bristol Myers Squibb elects to advance PRX019 after completion of the Phase 1 study, which could trigger a potential $55 million milestone by year-end 2026. (Prothena, 10-Q, May 2026)

· Whether PRTA continues repurchasing shares under the $100 million authorization or preserves cash as clinical timelines extend. (Prothena, 8-K, Feb. 2026; Prothena, 10-Q, May 2026)

· Whether any prospectus supplement, ATM activity, or other capital-markets filing follows the POS AM shelf update. (Prothena, POS AM, Feb. 2026)

· Whether Rubric, Scully, or other large 13G holders increase, reduce, or maintain exposure after future catalyst updates. (Prothena, Schedule 13G/A, May 2026)

· Whether Q2 and subsequent filings confirm that lower operating expenses are durable rather than simply restructuring-period timing effects. (Prothena, 10-Q, May 2026)

Market Tide Bottom Line

PRTA is not a simple turnaround, and it is not a clean profitability story. It is a well-funded, post-failure, event-driven biotech repositioning with partner-controlled upside, concentrated passive ownership, and a capital strategy that can either support the stock or add share-count pressure depending on what happens next. If partner milestones continue to arrive and management preserves capital discipline, the current setup could prove stronger than the market expects. If the milestone cadence slows, partners delay, or large holders reduce exposure, the same structure could amplify downside volatility. (Prothena, 10-K, Feb. 2026; Prothena, 10-Q, May 2026; Prothena, 8-K, Feb. 2026; Prothena, POS AM, Feb. 2026; Prothena, Schedule 13G/A, May 2026)

Required Disclosure

Market Tide Weekly is for informational and educational purposes only. Nothing in this newsletter constitutes investment advice, a solicitation to buy or sell any security, or a guarantee of any outcome. Past performance of featured picks is not indicative of future results. All investing involves risk, including the possible loss of principal. Readers should conduct their own due diligence and consult a qualified financial advisor before making investment decisions. Market Tide Weekly and its operators may hold positions in securities discussed.

Works Cited

Prothena Corporation plc. "Annual Report." Form 10-K. Prothena Corporation plc, 27 Feb. 2026.

Prothena Corporation plc. "Quarterly Report." Form 10-Q. Prothena Corporation plc, 7 May 2026.

Prothena Corporation plc. "Current Report: Full-Year 2025 and Fourth Quarter 2025 Results." Form 8-K. Prothena Corporation plc, 19 Feb. 2026.

Prothena Corporation plc. "Current Report: Share Repurchase Authorization." Form 8-K. Prothena Corporation plc, 27 Feb. 2026.

Prothena Corporation plc. "Post-Effective Amendment to Registration Statement." POS AM. Prothena Corporation plc, 27 Feb. 2026.

Prothena Corporation plc. "Definitive Proxy Statement." DEF 14A. Prothena Corporation plc, 27 Mar. 2026.

Prothena Corporation plc. "Additional Definitive Proxy Soliciting Materials." DEFA14A. Prothena Corporation plc, 27 Mar. 2026.

Prothena Corporation plc. "Current Report: First Quarter 2026 Results." Form 8-K. Prothena Corporation plc, 7 May 2026.

Prothena Corporation plc. "Current Report: Annual General Meeting Results." Form 8-K. Prothena Corporation plc, 15 May 2026.

Rubric Capital Management LP and David Rosen. "Schedule 13G/A Beneficial Ownership Statement." Schedule 13G/A. Prothena Corporation plc, 15 May 2026.

Scully, William P. "Schedule 13G/A Beneficial Ownership Statement." Schedule 13G/A. Prothena Corporation plc, 11 May 2026.

Prothena Corporation plc. "Current Report: Board Resignation." Form 8-K. Prothena Corporation plc, 10 Dec. 2025.

Prothena Corporation plc. "Current Report: Extraordinary General Meeting and Distributable Reserves." Form 8-K. Prothena Corporation plc, 19 Nov. 2025.