What the Filings Say That the Headlines Don’t

Market Tide Weekly — Tuesday Edition June 23, 2026

Reader Mode: This week’s picks are companies where the filings tell a better story than the headline numbers.

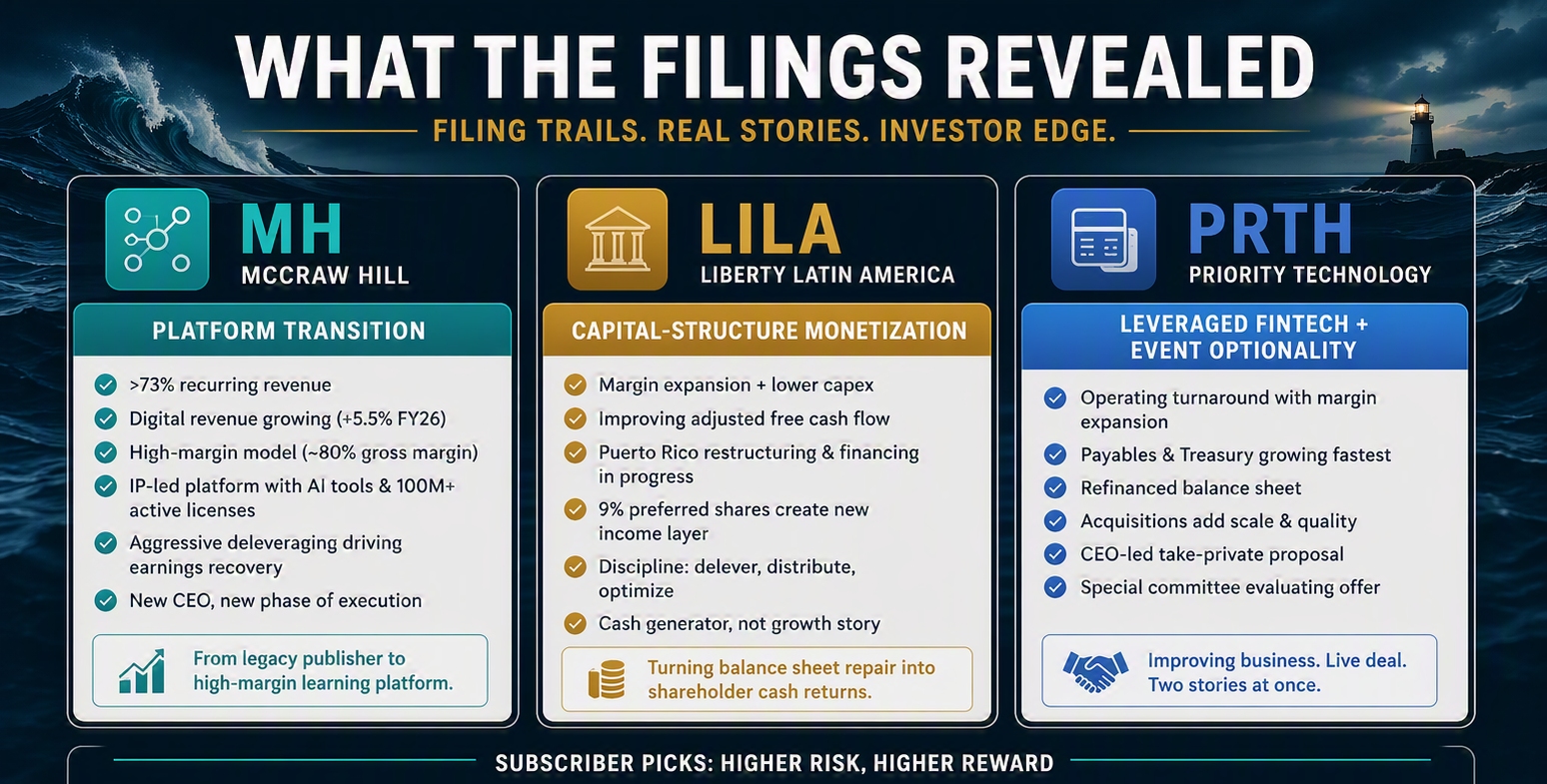

Public picks: McGraw Hill is shifting toward a recurring, digital education platform; Liberty Latin America is turning telecom repair into a capital-structure story; and Priority Technology is combining margin expansion with take-private optionality (McGraw Hill, Form 10-K; Liberty Latin America, Form 10-K; Priority Technology, Form 10-K).

Subscriber picks: 4D Molecular Therapeutics is the higher-risk biotech catalyst setup, and Nuveen Churchill Direct Lending is the income-reset monitor (4D Molecular Therapeutics, Form 10-K; Nuveen Churchill Direct Lending, Form 10-K).

Why This Week Matters

The screen gave us a list. The filings told us which names actually mattered. Several companies cleared the basic size and price filters, but only a few had a real story underneath the numbers. The best candidates this week were companies in transition: debt being repriced, cash flow being redirected, margins improving despite weak headline growth, and management teams moving from repair mode into execution mode.

That’s the theme of this issue: the headline number is not the story. For the public slate, we want ideas that are readable in one sitting but supported by a real filing trail. For subscribers, we keep the more complex risk/reward setups behind the email layer.

Public Pick 1 — MH: McGraw Hill

Setup: McGraw Hill looks flat on the surface. FY2026 revenue was roughly unchanged at about $2.1B. But the filing trail says the business underneath is getting better: more than 73% of revenue is recurring, digital revenue is growing, adjusted EBITDA margins are in the mid-30s, and net income flipped positive after a prior-year loss (McGraw Hill, Form 10-K; McGraw Hill, June 11 8-K).

Why it screens well: MH is not a textbook-publisher story anymore. It is a high-margin education business trying to become a platform. Higher Education is the growth engine; K-12 is the noisy, cyclical drag. That mix makes headline revenue look uninspiring, but Q3 showed the underlying model working: recurring revenue accelerated, digital revenue grew double digits, gross margin reached the mid-80% range, and debt kept coming down (McGraw Hill, Feb. 11 8-K; McGraw Hill, Form 10-Q).

The filing trail: The IPO was the starting line. It was not mainly about funding growth; it was about fixing the balance sheet. MH used IPO proceeds to repay debt, then repriced the remaining term loan, cut the spread from SOFR + 3.25% to SOFR + 2.75%, and kept paying down principal with cash flow. The CEO transition then put a new leadership structure on top of a cleaner financial base (McGraw Hill, IPO Closing 8-K; McGraw Hill, Sept. 8 8-K; McGraw Hill, Oct. 16 8-K; McGraw Hill, Dec. 30 8-K).

MTW read: MH is the cleanest “hidden transition” story this week. The bull case is that the market still sees a legacy publisher while the filings show a recurring, digital, AI-enabled education platform with improving earnings power. The bear case is that revenue growth is still too thin, K-12 can keep disrupting the story, and part of the earnings recovery comes from lower interest expense rather than pure operating acceleration.

Public Pick 2 — LILA: Liberty Latin America

Setup: Liberty Latin America is not a clean growth story. It is a leveraged telecom operator trying to turn operating repair into shareholder value. At its core, LILA is shifting from a growth story to a cash-harvesting and capital-allocation story. The filings point to margin expansion, lower capex, improving adjusted free cash flow, Puerto Rico stabilization, and a new preferred-share structure that changes how investors get paid (Liberty Latin America, Form 10-K; Liberty Latin America, May 7 8-K; Liberty Latin America, May 21 8-K).

Why it screens well: LILA’s revenue is not doing much. The cash-flow profile is. FY2025 showed stronger Adjusted OIBDA, better adjusted free cash flow, and tighter capex. Q1 2026 showed the recovery holding, even if unevenly. Puerto Rico remains the swing factor, but the filings show management isolating, financing, and trying to repair that risk instead of ignoring it (Liberty Latin America, Form 10-K; Liberty Latin America, May 7 8-K; Liberty Latin America, Sept. 25 8-K).

The filing trail: The sequence is the story: Puerto Rico impairment, more segment-level disclosure, high-cost Puerto Rico financing, FY2025 turnaround validation, Q1 2026 confirmation, and then the 9% Series A preferred-share distribution. That preferred layer gives holders a new income-producing security, but it also adds a fixed claim above the common stock (Liberty Latin America, Aug. 7 8-K; Liberty Latin America, Sept. 25 8-K; Liberty Latin America, Feb. 18 8-K; Liberty Latin America, May 21 8-K).

MTW read: LILA is messy, but the mess is the opportunity. The bull case is that management has stabilized enough cash flow to support preferred dividends, buybacks, and continued value extraction. The bear case is that leverage, refinancing risk, preferred-stock complexity, and Puerto Rico or weather-related volatility still have the power to swamp the recovery.

Public Pick 3 — PRTH: Priority Technology

Setup: Priority Technology is now two stories at once: an improving operating business and a live take-private situation. The operating business is improving, with revenue growth, margin expansion, stronger adjusted EBITDA, and better earnings. At the same time, a CEO-led take-private proposal adds an event-driven overlay (Priority Technology, Form 10-K; Priority Technology, May 11 8-K; Priority Technology, Nov. 10 8-K).

Why it screens well: PRTH has moved from “can it refinance?” to “can it grow into the debt?” The company reset its credit structure, added acquisition capacity, bought vertical merchant assets, and then showed Payables and Treasury growing faster than the legacy Merchant Solutions segment. The margin mix is the point: higher-quality revenue is helping EBITDA scale (Priority Technology, July 8 8-K; Priority Technology, Aug. 4 8-K; Priority Technology, Oct. 1 8-K; Priority Technology, May 11 8-K).

The filing trail: PRTH’s filings tell a three-part story: refinance the balance sheet, prove the operating model, then introduce take-private optionality. The July and August credit filings bought time. The 2025 results validated margin expansion. The CEO-led proposal created a possible cash-exit path, with a special committee process now sitting on top of the standalone thesis (Priority Technology, July 8 8-K; Priority Technology, Aug. 4 8-K; Priority Technology, Mar. 10 8-K; Priority Technology, Nov. 10 8-K).

MTW read: PRTH is easy to describe but hard to price: growing payments platform, heavy leverage, improving margins, and a live deal process. The bull case is that EBITDA keeps compounding and the business is worth more than the initial proposal suggests. The bear case is that leverage, integration risk, SMB transaction exposure, and deal uncertainty keep the equity volatile.

Thursday Deep Dive Preview — MH

MH deserves the Thursday Deep Dive because it has the cleanest full arc of the week: IPO structure, debt repayment, lender repricing, repeated cash paydowns, Q1 baseline, Q2 divergence, Q3 proof point, FY2026 profitability, and a CEO/governance handoff into execution mode. The key question for Thursday is simple: is MH still a flat legacy publisher, or is it a high-margin subscription education platform the market has not fully re-rated? (McGraw Hill, IPO Closing 8-K; McGraw Hill, Sept. 8 8-K; McGraw Hill, Oct. 16 8-K; McGraw Hill, Feb. 11 8-K; McGraw Hill, June 11 8-K).

Visual Anchor

What the Filings Revealed

| Category | MH | LILA | PRTH |

|----------|----|------|------|

| Core Thesis | Platform Transition | Capital-Structure Monetization | Leveraged Fintech + Event Optionality |

CTA / Share Layer

If this helped you see past the headline numbers, send it to someone who still reads earnings releases instead of filings. Subscribers get the catalyst framework on FDMT and the income reset playbook on NCDL. Thursday: we break down McGraw Hill’s full IPO-to-platform transition.

Disclosure

This edition is based on the filing summaries and operator-reviewed notes assembled above. It is not investment advice. The operator has confirmed no current positions in FDMT, LILA, MH, NCDL, or PRTH.

Sources

4D Molecular Therapeutics, Inc. Form 10-K for the Fiscal Year Ended December 31, 2025. U.S. Securities and Exchange Commission, 2026.

4D Molecular Therapeutics, Inc. Current Reports on Form 8-K: Otsuka Collaboration, PRISM Clinical Update, Financing, Leadership, Phase 3 Protocol, Q1 2026 Results, and Annual Meeting Updates. U.S. Securities and Exchange Commission, 2025–2026.

Liberty Latin America Ltd. Form 10-K for the Fiscal Year Ended December 31, 2025. U.S. Securities and Exchange Commission, 2026.

Liberty Latin America Ltd. Current Reports on Form 8-K: Puerto Rico Impairment, Secured Credit Facility, FY2025 Results, Q1 2026 Results, Preferred Share Distribution, and Segment Reports. U.S. Securities and Exchange Commission, 2025–2026.

McGraw Hill, Inc. Form 10-K for Fiscal Year 2026. U.S. Securities and Exchange Commission, 2026.

McGraw Hill, Inc. Form 10-Q for the Quarter Ended December 31, 2025. U.S. Securities and Exchange Commission, 11 Feb. 2026.

McGraw Hill, Inc. Current Reports on Form 8-K: IPO Closing, Debt Repricing, Credit Agreement Amendment, Debt Repayments, Q1–Q4/FY2026 Earnings Releases, CEO Succession, and Governance/Compensation Updates. U.S. Securities and Exchange Commission, 2025–2026.

Nuveen Churchill Direct Lending Corp. Form 10-K for the Fiscal Year Ended December 31, 2025. U.S. Securities and Exchange Commission, 2026.

Nuveen Churchill Direct Lending Corp. Current Reports on Form 8-K: Q2 2025 Results, Q3 2025 Results, Q4/FY2025 Results, Dividend Reset, Share Repurchase Plan, Q1 2026 Results, and Annual Meeting Results. U.S. Securities and Exchange Commission, 2025–2026.

Priority Technology Holdings, Inc. Form 10-K for the Fiscal Year Ended December 31, 2025. U.S. Securities and Exchange Commission, 2026.

Priority Technology Holdings, Inc. Current Reports on Form 8-K: Credit Facility Launch, Credit Agreement Amendment, Acquisitions, Q3 2025 Results, CEO-Led Take-Private Proposal, Special Committee Process, FY2025 Results, Auditor Change, and Q1 2026 Results. U.S. Securities and Exchange Commission, 2025–2026.