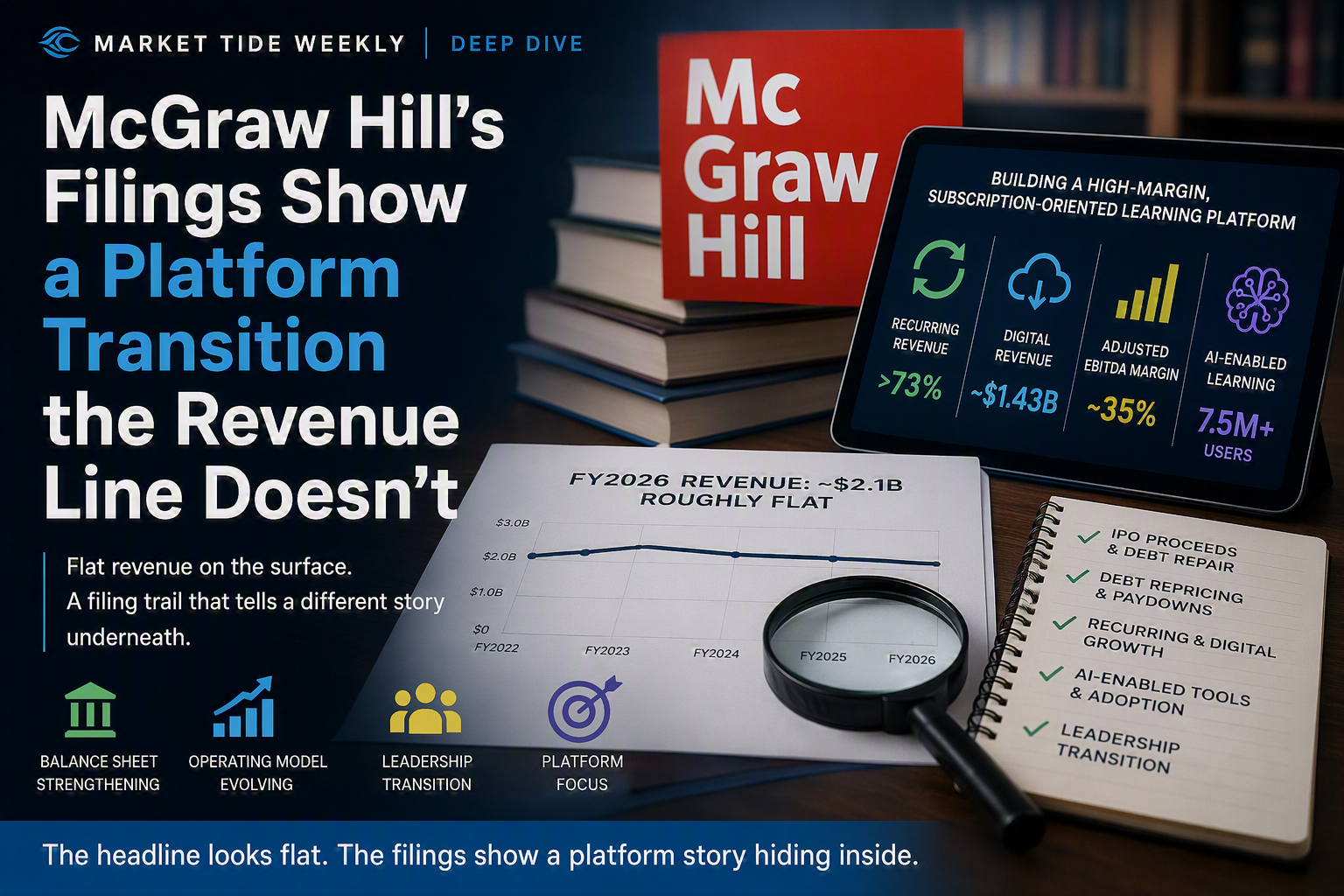

McGraw Hill’s Filings Show a Platform Transition the Revenue Line Doesn’t

The revenue line is flat. The business model isn’t.

The headline number looks flat. The filings show a post-IPO education company using debt repair, recurring revenue, digital adoption, and leadership transition to push beyond the legacy-publisher label.

MARKET TIDE WEEKLY DEEP DIVE -MCGRAW HILL, INC.

McGraw Hill is easy to misread if the analysis stops at the headline number. FY2026 revenue was roughly flat, which makes the company look like a slow-moving legacy publisher at first glance. But the filing trail points to a more interesting transition: a newly public education company using IPO proceeds, debt repayment, loan repricing, recurring revenue growth, digital mix shift, and leadership succession to move toward a high-margin, subscription-oriented learning platform. The central question for investors is whether the market is still pricing MH like a flat textbook business while the filings show a platform transition and balance-sheet repair story unfolding underneath. (McGraw Hill, 424B4 Prospectus, July 2025; McGraw Hill, Form 10-K, FY2026; McGraw Hill, CEO Succession 8-K, Jan. 2026)

This week’s question: can a company look flat on the surface while fundamentally changing underneath?

Executive Summary

· Core thesis: MH is a filing-led reclassification story, not a conventional revenue-growth story. Flat FY2026 revenue masks a business increasingly shaped by recurring, digital, high-margin learning products. (McGraw Hill, Form 10-K, FY2026; McGraw Hill, FY2026 Earnings 8-K, June 2026)

· Balance-sheet reset: The 424B4 prospectus and post-IPO 8-K sequence show MH using IPO proceeds, loan repricing, and repeated debt repayments to lower leverage and reduce interest expense. (McGraw Hill, 424B4 Prospectus, July 2025; McGraw Hill, Credit Agreement 8-K, Sept. 2025; McGraw Hill, Debt Repayment 8-K, Oct. 2025; McGraw Hill, Debt Repayment 8-K, Dec. 2025)

· Operating evidence: Q3 and FY2026 filings show recurring revenue growth, digital revenue growth, Higher Education strength, high adjusted EBITDA margins, positive net income, and early signals of an AI-enabled learning platform. (McGraw Hill, Form 10-Q, Feb. 2026; McGraw Hill, Form 10-K, FY2026; McGraw Hill, FY2026 Earnings 8-K, June 2026)

· Key risks: K-12 cyclicality, weak headline growth, sponsor-control optics, and the possibility that earnings improvement is viewed as balance-sheet repair rather than operating acceleration remain the main constraints on a faster reclassification. (McGraw Hill, Form 10-K, FY2026; McGraw Hill, 424B4 Prospectus, July 2025)

· MTW takeaway: MH belongs on the watch list because the structure underneath the headline is changing. The question is whether management can make the platform transition visible enough for the market to stop treating the company like a flat legacy publisher. (McGraw Hill, Form 10-K, FY2026; McGraw Hill, FY2026 Earnings 8-K, June 2026)

1. The Setup

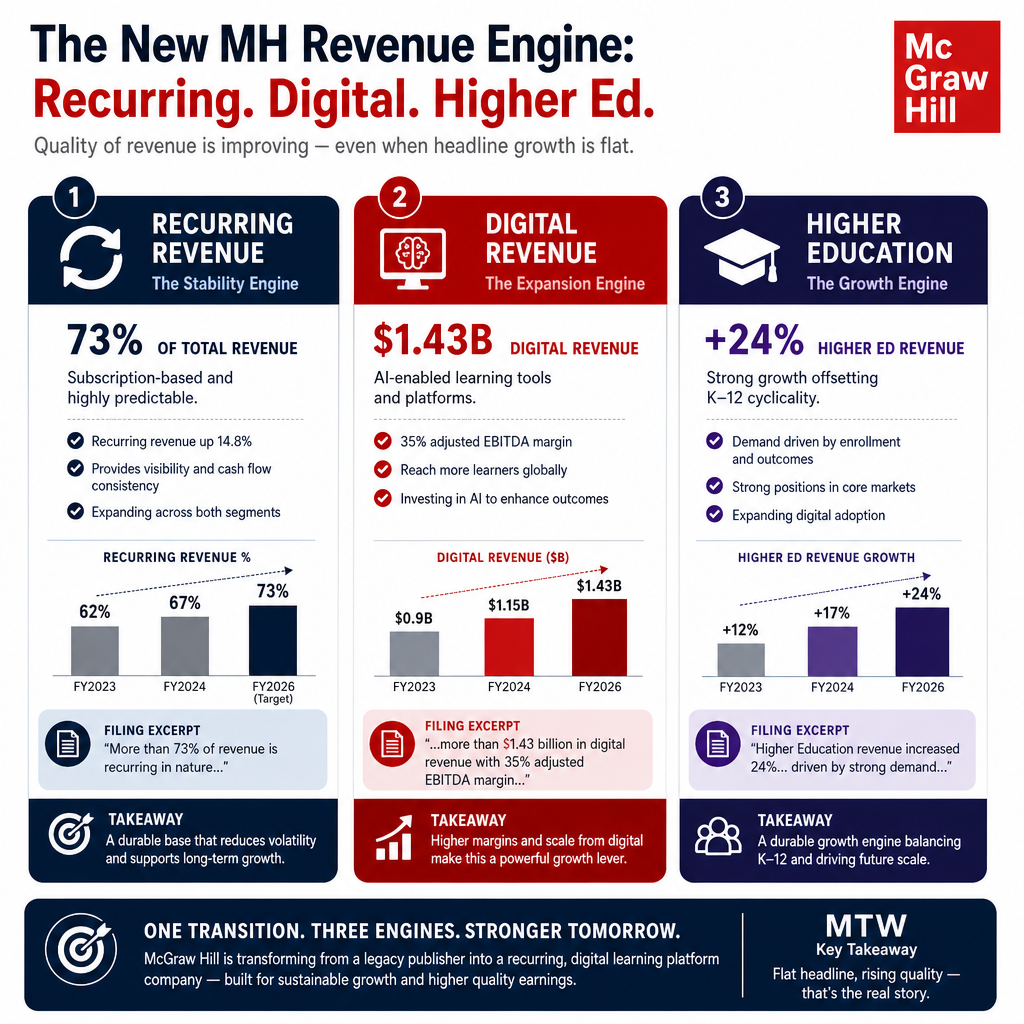

The setup for MH is straightforward: the headline looks muted, but the filings are more revealing. FY2026 revenue was roughly flat at about $2.1 billion, which makes McGraw Hill look like a slow-growth education publisher if the analysis stops there. But the filing trail points to a higher-quality business forming underneath the flat top line. More than 73% of revenue is recurring, digital revenue continues to grow, adjusted EBITDA margins sit in the mid-30% range, net income turned positive after a prior-year loss, and management kept reducing debt after the IPO. (McGraw Hill, Form 10-K, FY2026; McGraw Hill, FY2026 Earnings 8-K, June 2026)

The data triad is the point: more than 73% recurring revenue, roughly 35% adjusted EBITDA margins, and a rising digital mix now define the model investors have to evaluate. (McGraw Hill, Form 10-K, FY2026; McGraw Hill, FY2026 Earnings 8-K, June 2026)

McGraw Hill has been riding the tide for several weeks, and we have been watching the filing trail develop in real time. As each new disclosure added another layer — IPO proceeds, debt repricing, cash paydowns, recurring revenue growth, digital adoption, and leadership transition — we adjusted the pressure and went deeper. What started as a flat-revenue education name became a fuller transition story once the filings were read in sequence. (McGraw Hill, 424B4 Prospectus, July 2025; McGraw Hill, Credit Agreement 8-K, Sept. 2025; McGraw Hill, Debt Repayment 8-K, Oct. 2025; McGraw Hill, Form 10-Q, Feb. 2026; McGraw Hill, FY2026 Earnings 8-K, June 2026)

That makes MH a natural fit for this week’s theme: the headline number is not the story. The important evidence is spread across a filing sequence rather than captured in one clean growth metric. The 424B4 prospectus and IPO closing 8-K show the company entering the public markets with debt repayment built into the transaction. The Sept. 8 credit-agreement amendment, the Oct. 16 repayment, and the Dec. 10 repayment show the balance-sheet repair continuing after the IPO. The Feb. 11 Q3 filing shows the operating model beginning to prove itself, while the June 11 FY2026 materials confirm that profitability, recurring revenue, digital revenue, and AI-enabled learning tools are now central to the company’s public story. (McGraw Hill, 424B4 Prospectus, July 2025; McGraw Hill, IPO Closing 8-K, July 2025; McGraw Hill, Credit Agreement 8-K, Sept. 2025; McGraw Hill, Debt Repayment 8-K, Oct. 2025; McGraw Hill, Debt Repayment 8-K, Dec. 2025; McGraw Hill, Form 10-Q, Feb. 2026; McGraw Hill, FY2026 Earnings 8-K, June 2026)

The Deep Dive therefore starts with a question the headline revenue number cannot answer: is MH still a flat legacy textbook company, or is it becoming a high-margin, recurring, digital learning platform that the market has not fully reclassified yet? That question is what the filings allow us to test. (McGraw Hill, Form 10-K, FY2026)

2. The Filing Evidence

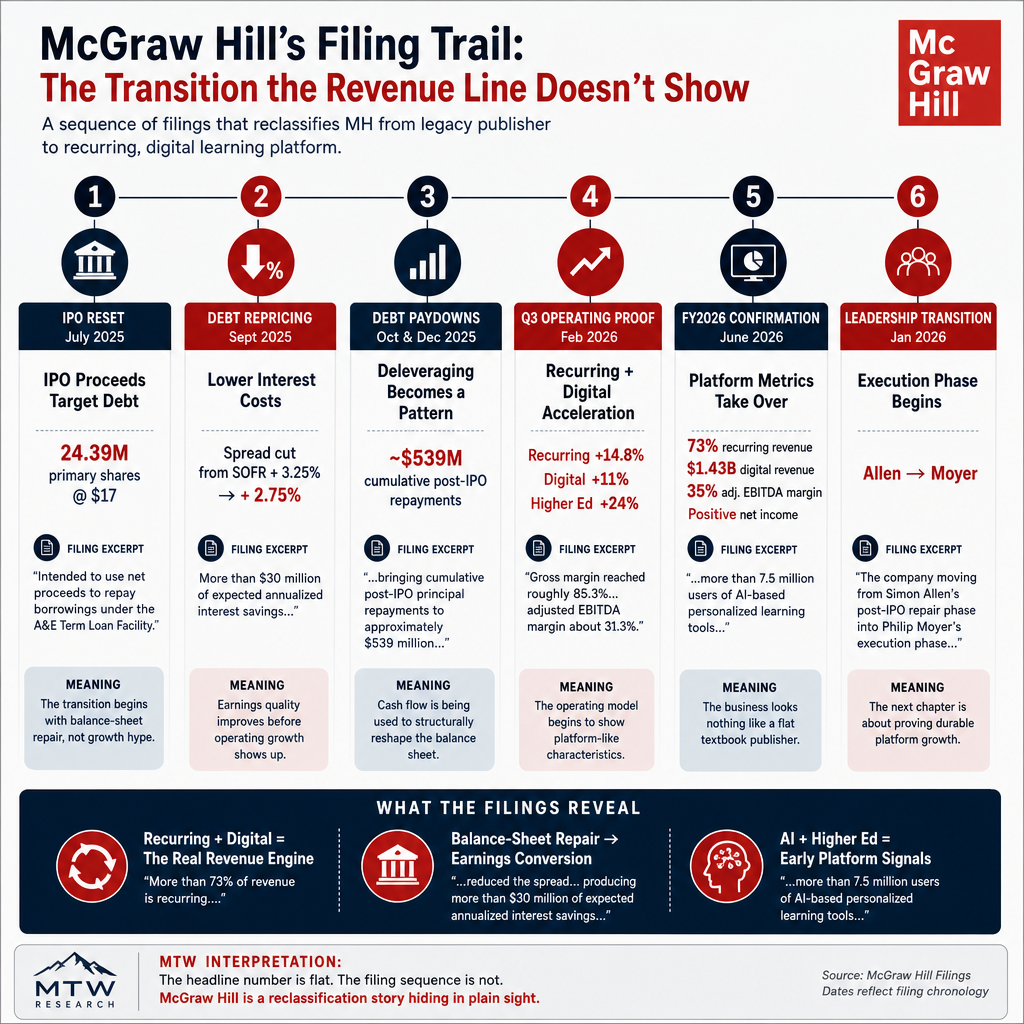

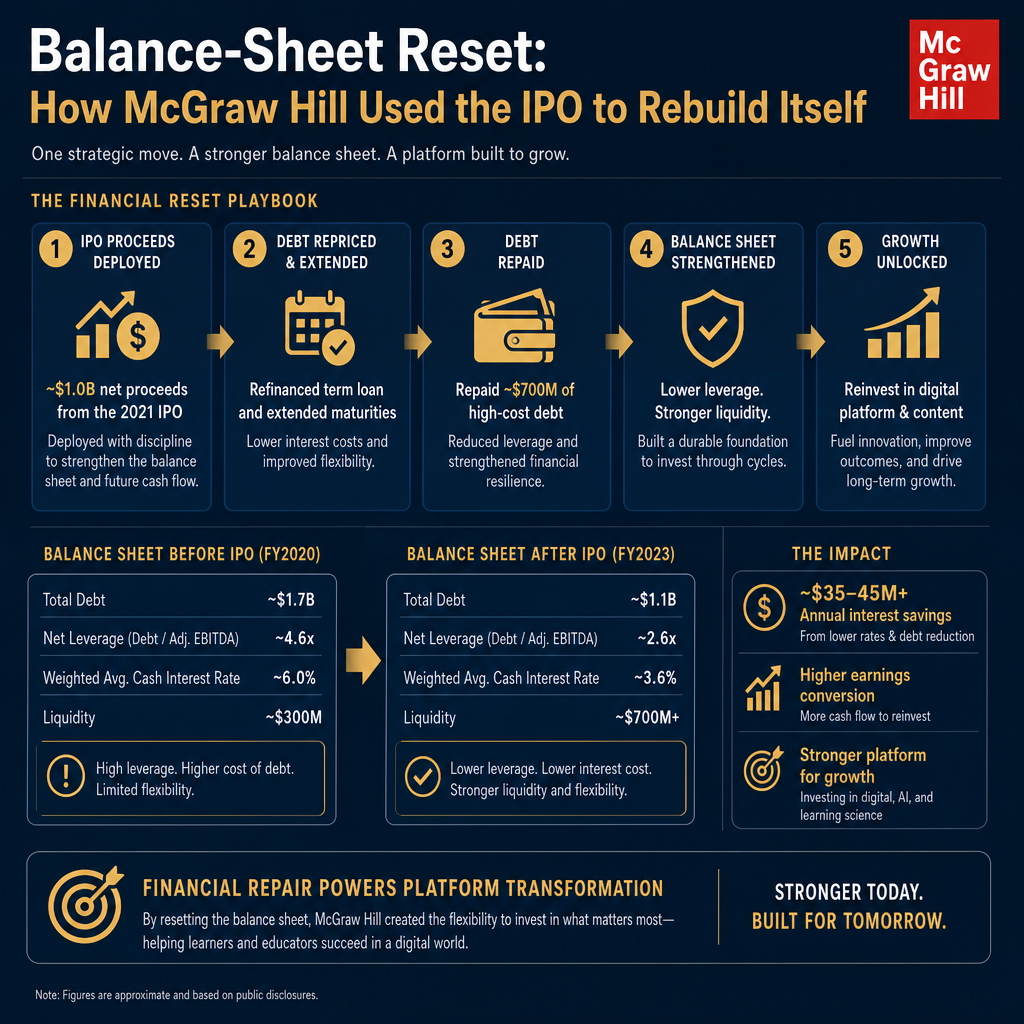

The filing trail starts with the IPO itself. The 424B4 prospectus states that McGraw Hill offered 24.39 million primary shares at $17.00 per share and intended to use net proceeds to repay borrowings under the A&E Term Loan Facility. That matters because it frames the public-company story correctly: MH did not come public simply to fund an aggressive growth push. It came public with balance-sheet repair built into the transaction from day one. (McGraw Hill, 424B4 Prospectus, July 2025)

The prospectus also adds a governance caution. The selling stockholder could sell up to 3.6585 million additional shares through the underwriters’ over-allotment option, with MH receiving no proceeds from those shares. At the same time, PE Mav Holdings, LLC, an investment vehicle of funds sponsored and controlled by Platinum Equity, LLC, was expected to retain about 86.5% of voting power after the offering, making MH a controlled company under NYSE rules. Public investors were therefore buying into the transition, but not controlling it. (McGraw Hill, 424B4 Prospectus, July 2025)

The next filings show that the debt story did not stop at the IPO. In September, MH completed a credit-agreement repricing that reduced the spread on its remaining term loan from SOFR + 3.25% to SOFR + 2.75%, producing more than $30 million of expected annualized interest savings from the repricing alone. In October, the company followed with a $150 million term-loan repayment, bringing cumulative post-IPO principal repayments to approximately $539 million and leaving roughly $618 million outstanding. The December filing added another $50 million paydown, reinforcing that deleveraging was becoming a repeatable cash-flow use rather than a one-time IPO event. By year-end, management also highlighted roughly $645 million of debt reduction, while the Oct. 16 filing had already shown approximately $539 million of cumulative post-IPO principal repayments. (McGraw Hill, Credit Agreement 8-K, Sept. 2025; McGraw Hill, Debt Repayment 8-K, Oct. 2025; McGraw Hill, Debt Repayment 8-K, Dec. 2025; McGraw Hill, Form 10-K, FY2026)

The Q1 and Q2 filings fill in the operating transition between the IPO reset and the Q3 proof point. Q1 established the post-IPO baseline: modest headline growth, recurring and digital revenue growing faster than total revenue, strong adjusted EBITDA, high gross margin, and only minimal GAAP profitability. Q2 then showed the key divergence: a smaller K-12 market pulled headline revenue lower even as recurring revenue, digital revenue, Higher Education strength, gross-margin expansion, and raised guidance continued to support the platform thesis. (McGraw Hill, Q1 Earnings 8-K, Aug. 2025; McGraw Hill, Q2 Earnings 8-K, Nov. 2025)

The operating evidence then begins to catch up with the financial reset. The Feb. 11 Form 10-Q explicitly shows revenue up about 4.2%, recurring revenue up about 14.8%, digital revenue up about 11.0%, and Higher Education up about 24%. Gross margin reached roughly 85.3%, adjusted EBITDA margin was about 31.3%, and the company prepaid another $200 million of debt during the quarter. That quarter is important because it connected the two halves of the thesis: the business mix was improving while the balance sheet was still being repaired. (McGraw Hill, Form 10-Q, Feb. 2026; McGraw Hill, Q3 Earnings 8-K, Feb. 2026)

The June 11 FY2026 8-K confirms the same pattern. FY2026 revenue was roughly flat, but recurring revenue represented more than 73% of total revenue, digital revenue reached about $1.43 billion, adjusted EBITDA was about $744 million, adjusted EBITDA margin was around 35%, and net income turned positive at roughly $35 million after a prior-year loss. The June year-end release also highlighted more than 7.5 million users of AI-based personalized learning tools and more than 100 million active curriculum licenses globally, supporting the idea that MH is trying to reposition itself as an AI-enabled learning platform rather than a legacy textbook publisher. (McGraw Hill, Form 10-K, FY2026; McGraw Hill, FY2026 Earnings 8-K, June 2026)

The final piece of the filing sequence is leadership. The Dec. 30 CEO succession filing and Jan. 5 governance and compensation implementation filing show the company moving from Simon Allen’s post-IPO repair phase into Philip Moyer’s execution phase, with Allen remaining Chairman and the new leadership structure formalized through compensation, board, and employment arrangements. That handoff matters because the easy part of the story may already be behind MH: raise equity, repay debt, reprice debt, and show margin strength. The harder part now is proving that recurring, digital, and AI-enabled learning revenue can drive a durable public-company growth profile. (McGraw Hill, CEO Succession 8-K, Jan. 2026; McGraw Hill, Governance and Compensation 8-K, Jan. 2026)

3. The Opportunity or Risk

The filing trail allows a different interpretation than the headline revenue suggests: McGraw Hill may already be operating like a higher-quality platform business, even if the market has not yet recognized it. MH’s opportunity is not built on explosive top-line growth. It is built on the possibility of market reclassification. The company still looks flat if investors stop at FY2026 revenue, which was roughly unchanged. But the filings show a higher-quality business forming underneath that headline: recurring revenue is a larger share of the mix, digital revenue is growing faster than total revenue, adjusted EBITDA margins remain high, and the balance sheet is improving after the IPO. (McGraw Hill, Form 10-K, FY2026; McGraw Hill, FY2026 Earnings 8-K, June 2026)

The central opportunity is that the market may still be valuing MH like a legacy textbook publisher while the filing trail points toward a recurring, digital, AI-enabled education platform. That distinction matters because platform-like revenue deserves more attention than a cyclical print-heavy business, especially if Higher Education continues to carry growth while K-12 volatility masks the underlying progress. (McGraw Hill, Form 10-K, FY2026; McGraw Hill, Form 10-Q, Feb. 2026)

The financial side of the opportunity is equally important. The 424B4 prospectus shows that the IPO was designed around term-loan repayment, and the later filing sequence shows management using the public-company reset to keep lowering debt and interest expense. The Sept. 8 repricing, the Oct. 16 repayment, and the Dec. 10 repayment all point in the same direction: lower financing costs, better earnings conversion, and a cleaner path for operating improvements to show up in net income. (McGraw Hill, 424B4 Prospectus, July 2025; McGraw Hill, Credit Agreement 8-K, Sept. 2025; McGraw Hill, Debt Repayment 8-K, Oct. 2025; McGraw Hill, Debt Repayment 8-K, Dec. 2025)

The operating upside depends on whether MH can prove that its strongest segments and products are more durable than the headline revenue number suggests. Higher Education appears to be the growth engine, while recurring and digital products are shifting the company away from a purely transactional publishing model. If AI-enabled learning tools improve adoption, engagement, retention, or pricing power, the market may eventually view MH less as a textbook company and more as a high-margin learning infrastructure provider. (McGraw Hill, Form 10-Q, Feb. 2026; McGraw Hill, FY2026 Earnings 8-K, June 2026)

The re-rating condition is straightforward but demanding: MH has to keep growing recurring and digital revenue, continue deleveraging, sustain Higher Education momentum, and show that AI-enabled products are commercially meaningful rather than just strategically interesting. If those pieces hold together, the filings suggest a company that could look very different from the legacy-publisher label investors may still attach to it. (McGraw Hill, Form 10-K, FY2026; McGraw Hill, FY2026 Earnings 8-K, June 2026)

The interpretive gap is simple: the filings describe a recurring, margin-rich platform, while the market still sees a flat textbook business. (McGraw Hill, Form 10-K, FY2026; McGraw Hill, FY2026 Earnings 8-K, June 2026)

4. Risks to the Thesis

MH’s risk profile starts with the same fact that makes the thesis interesting: this is not a clean growth story. The company’s FY2026 revenue was roughly flat, so the bull case depends on investors looking past the headline and giving credit for better revenue quality, stronger margins, recurring digital mix, debt reduction, and improved earnings conversion. If the market continues to focus on total revenue growth alone, MH may remain valued like a legacy education publisher rather than a high-margin learning platform. (McGraw Hill, Form 10-K, FY2026)

The most immediate operating risk is K-12 cyclicality. K-12 revenue remains tied to procurement cycles, school funding, adoption schedules, and changes in market size. That volatility can keep obscuring the progress MH is making in recurring and digital revenue, especially if Higher Education remains the main growth engine while K-12 periodically pulls the headline number lower. A platform-style re-rating becomes harder if investors cannot separate durable digital learning demand from cyclical school-adoption noise. (McGraw Hill, Form 10-K, FY2026; McGraw Hill, Form 10-Q, Feb. 2026)

There is also a balance-sheet repair perception risk. The filing trail shows real improvement, but a meaningful portion of the earnings recovery comes from debt repayment, loan repricing, and lower interest expense. That is constructive, but it also means investors may discount the improvement if operating growth does not strengthen. MH needs recurring revenue, digital adoption, Higher Education momentum, and AI-enabled product value to become visible enough that the story is not reduced to “lower interest expense after the IPO.” (McGraw Hill, 424B4 Prospectus, July 2025; McGraw Hill, Credit Agreement 8-K, Sept. 2025; McGraw Hill, Debt Repayment 8-K, Oct. 2025; McGraw Hill, Debt Repayment 8-K, Dec. 2025)

Leadership transition adds another execution test. Philip Moyer inherits a cleaner financial base, while Simon Allen’s move to Chairman preserves continuity, but the next phase is harder than the first phase. Management must sustain Higher Education momentum, stabilize K-12 performance, prove that AI-enabled tools are more than marketing language, and maintain deleveraging discipline after the easiest post-IPO balance-sheet actions have already been completed. (McGraw Hill, CEO Succession 8-K, Jan. 2026; McGraw Hill, Governance and Compensation 8-K, Jan. 2026)

AI adoption adds a related proof-point risk. The June 11 FY2026 materials highlighted more than 7.5 million users of AI-based personalized learning tools and more than 100 million active curriculum licenses globally, but those figures do not yet prove monetization, retention lift, pricing power, or margin durability. Management still has to show whether AI-enabled tools improve adoption, engagement, renewal behavior, or reported results in ways investors can measure. Until then, AI should be treated as an important watch item, not a completed proof point. (McGraw Hill, Form 10-K, FY2026; McGraw Hill, FY2026 Earnings 8-K, June 2026)

Finally, the 424B4 prospectus adds a governance and ownership risk. Platinum-linked holders retained significant voting control after the IPO, and the selling-stockholder over-allotment structure showed that public investors were entering alongside sponsor monetization rather than replacing sponsor control. That does not negate the operating thesis, but it does mean minority shareholders have limited influence over governance outcomes, and future secondary-sale pressure or controlled-company optics could weigh on sentiment. (McGraw Hill, 424B4 Prospectus, July 2025)

5. MTW Bottom Line

MTW’s bottom line: MH is not a momentum growth story; it is a filing-led reclassification story. The market can still look at roughly flat FY2026 revenue and see a legacy publisher, but the filings show a different structure forming underneath: recurring revenue above 73% of total revenue, growing digital adoption, high adjusted EBITDA margins, repeated debt reduction, lower interest burden, and a leadership handoff into the next execution phase. If management can sustain recurring revenue growth, continue deleveraging, and demonstrate that AI-enabled tools drive measurable adoption or pricing power, the market may begin to reclassify McGraw Hill over time. That outcome, however, remains dependent on execution, K-12 stability, and continued visibility into operating, not just financial, improvement. For now, MH belongs on the watch list as a filing-led transition story: not because the headline numbers are exciting, but because the structure underneath them is changing. (McGraw Hill, 424B4 Prospectus, July 2025; McGraw Hill, Form 10-K, FY2026; McGraw Hill, Credit Agreement 8-K, Sept. 2025; McGraw Hill, FY2026 Earnings 8-K, June 2026; McGraw Hill, CEO Succession 8-K, Jan. 2026; McGraw Hill, Governance and Compensation 8-K, Jan. 2026)

Watch-list action: Keep MH on the pressure board. The next checks are whether recurring and digital revenue keep expanding, whether Higher Education momentum offsets K-12 volatility, whether AI-enabled tools begin showing measurable adoption or pricing power, and whether management continues to use cash flow to reduce leverage rather than simply relying on the post-IPO reset. (McGraw Hill, Form 10-K, FY2026; McGraw Hill, FY2026 Earnings 8-K, June 2026)

Sources

McGraw Hill, Inc. Prospectus Filed Pursuant to Rule 424(b)(4), Initial Public Offering. McGraw Hill, Inc., 24 July 2025, /MTW/SEC_Filings/MH/424B4/2025-07-24/, No. 0001628280-25-035928.

McGraw Hill, Inc. Form 10-K for Fiscal Year 2026. McGraw Hill, Inc., 11 June 2026, /MTW/SEC_Filings/MH/10-K/2026-06-11/, No. 0001951070-26-000022.

McGraw Hill, Inc. Form 10-Q for the Quarter Ended December 31, 2025. McGraw Hill, Inc., 11 Feb. 2026, /MTW/SEC_Filings/MH/10-Q/2026-02-11/, No. 0001951070-26-000011.

McGraw Hill, Inc. Current Report on Form 8-K: IPO Closing. McGraw Hill, Inc., 25 July 2025, /MTW/SEC_Filings/MH/8-K/2025-07-25/, No. 0001628280-25-036062.

McGraw Hill, Inc. Current Report on Form 8-K: Fiscal Q1 2026 Earnings. McGraw Hill, Inc., 14 Aug. 2025, /MTW/SEC_Filings/MH/8-K/2025-08-14/, No. 0001628280-25-040279.

McGraw Hill, Inc. Current Report on Form 8-K: Fiscal Q2 2026 Earnings. McGraw Hill, Inc., 12 Nov. 2025, /MTW/SEC_Filings/MH/8-K/2025-11-12/, No. 0001951070-25-000008.

McGraw Hill, Inc. Current Report on Form 8-K: Debt Repricing Process. McGraw Hill, Inc., 2 Sept. 2025, /MTW/SEC_Filings/MH/8-K/2025-09-02/, No. 0001193125-25-193517.

McGraw Hill, Inc. Current Report on Form 8-K: Credit Agreement Amendment. McGraw Hill, Inc., 9 Sept. 2025, /MTW/SEC_Filings/MH/8-K/2025-09-09/, No. 0001193125-25-198855.

McGraw Hill, Inc. Current Report on Form 8-K: Term Loan Repayment. McGraw Hill, Inc., 16 Oct. 2025, /MTW/SEC_Filings/MH/8-K/2025-10-16/, No. 0001193125-25-241428.

McGraw Hill, Inc. Current Report on Form 8-K: Term Loan Repayment. McGraw Hill, Inc., 10 Dec. 2025, /MTW/SEC_Filings/MH/8-K/2025-12-10/, No. 0001193125-25-314229.

McGraw Hill, Inc. Current Report on Form 8-K: Fiscal Q3 2026 Earnings. McGraw Hill, Inc., 11 Feb. 2026, /MTW/SEC_Filings/MH/8-K/2026-02-11/, No. 0001951070-26-000010.

McGraw Hill, Inc. Current Report on Form 8-K: Fiscal Q4 and FY2026 Earnings. McGraw Hill, Inc., 11 June 2026, /MTW/SEC_Filings/MH/8-K/2026-06-11/, No. 0001951070-26-000021.

McGraw Hill, Inc. Current Report on Form 8-K: CEO Succession. McGraw Hill, Inc., 6 Jan. 2026, /MTW/SEC_Filings/MH/8-K/2026-01-06/, No. 0001193125-26-003463.

McGraw Hill, Inc. Current Report on Form 8-K: Governance and Compensation Implementation. McGraw Hill, Inc., 8 Jan. 2026, /MTW/SEC_Filings/MH/8-K/2026-01-08/, No. 0001193125-26-007781.